Stability in Uncertain Times: How Whole Life Insurance Supports Long-Term Business Goals

Whole life insurance is often misunderstood as just a personal safety net, but when you’re a business owner it can support your long-term goals: protecting key people,

Economic uncertainty is no longer a passing headline—it’s the backdrop every business leader is operating against. Market cycles are tightening, credit conditions can shift overnight, and succession and talent risks are more visible than ever. In this environment, long‑term planning isn’t just about chasing growth; it’s about building stability that can withstand shocks and support your goals over decades, not just quarters.

Whole life insurance is often viewed purely as a personal or family planning tool, but for businesses it can play a very different role: a source of guarantees, liquidity options, and continuity at moments when stability matters most. When structured thoughtfully, whole life can help protect key people, fund ownership transitions, and create a conservative asset that supports your broader strategy—not just your balance sheet.

Learn how whole life insurance can function as a stabilizing force inside your business: what it is, where it fits, and how it can support long‑term goals like succession, growth, and resilience. The goal is not to promote a product, but to help you see where this often‑misunderstood tool may, or may not, belong in your overall business planning.

Whole Life Insurance 101 – What You Need to Know

Before you decide whether whole life insurance belongs in your business plan, you need to understand what you’re actually working with. Whole life is a type of permanent life insurance: you pay premiums, you receive a guaranteed death benefit, and you build cash value inside the policy over time. As long as you follow the terms of the contract and keep premiums paid, the coverage is designed to last for your entire life—not just for a set number of years.

You can think of whole life as doing two things at once for you:

- It provides a guaranteed death benefit that can protect your business if you, a partner, or a key employee dies.

- It builds a cash value component that grows over time and can become a conservative asset on your personal or business balance sheet, depending on how you structure ownership.

This is very different from term insurance. With term coverage, you typically pay a lower premium for a set period—10, 20, or 30 years—and if you die during that term, your beneficiaries receive the death benefit. If you outlive the term, the coverage usually ends and you don’t build any cash value. Term can be an efficient way for you to cover temporary risks, but it doesn’t give you the long‑term guarantees or balance‑sheet presence that whole life can.

With whole life, you’re paying for a package of guarantees:

- A guaranteed death benefit (subject to the terms of the contract).

- Guaranteed cash value that grows according to the policy’s schedule.

- Level premiums that you can plan around.

On top of those guarantees, your policy may be eligible to receive dividends from the insurer. Dividends are not guaranteed, but when they are paid you can choose how to use them—such as reducing your out‑of‑pocket premiums, buying additional coverage, or increasing cash value.

When you look at whole life through this lens—not just as “insurance,” but as a long‑term contract that combines protection, guarantees, and potential cash value—you can start to see how it might support your broader business goals, not just your personal ones.

Create Stability Through Guaranteed Values

When you’re navigating uncertainty, you don’t just need growth—you need a foundation you can count on. The guarantees inside a whole life policy can help you create that foundation. The policy’s guaranteed cash value grows according to a schedule laid out in the contract, giving you a conservative asset you can plan around instead of one that swings with the markets. Over time, that cash value can become a quiet stabilizer on your business or personal balance sheet, depending on how you structure ownership.

You can also think of the cash value as a potential source of backup liquidity. Subject to the terms of the policy, you can typically access it through policy loans or withdrawals. That access is not “free money”—loans accrue interest, reduce available cash value, and can reduce the death benefit if not managed properly—but it can give you an option when you need flexibility and traditional credit is tight or slow to materialize.

By building this pool of guaranteed value, you create an internal reserve that you control. You can use it to help cover short-term cash flow gaps, weather a downturn, or seize an opportunity you don’t want to miss—such as a strategic hire, a discounted asset purchase, or a time-sensitive expansion. Instead of being forced to react on the terms of lenders or the market, you have one more lever you can pull on your own terms.

Over the long run, this stability can change how you plan. Rather than relying exclusively on lines of credit and more volatile investments, you can blend those tools with the guarantees of whole life insurance. That combination can help you pursue growth without leaving your business exposed to every bump in the economic road.

Protect Your Business: Key Uses of Whole Life Insurance

When you think about protecting your business, you probably think about cash flow, clients, and competition. But the real stress test often comes when something happens to a person—not a number—who holds the business together. Whole life insurance can give you a structured way to protect against those moments and keep your long‑term goals on track.

A. Key Person Coverage: Protecting the People You Rely On

Every business has a few people you simply can’t afford to lose—maybe that’s you, a partner, or a key executive who drives sales, relationships, or technical expertise. If one of those people dies unexpectedly, you’re not just facing an emotional loss; you’re also facing real financial disruption.

With key person coverage, your business owns a whole life policy on that individual and is the beneficiary of the death benefit. If that person dies, your company receives a lump sum that you can use to:

- Replace lost revenue tied directly to that person’s relationships or production.

- Cover the cost of recruiting, hiring, and onboarding a qualified replacement.

- Stabilize cash flow so you can meet payroll, service debt, and reassure stakeholders.

Because you’re using whole life, you’re not only getting a guaranteed death benefit; you’re also building cash value over time. That cash value can strengthen your balance sheet and provide you with another tool for managing risk and opportunity while that key person is still alive and working in the business.

B. Funding Buy–Sell Agreements: Keeping Control and Continuity

If you own your business with one or more partners, you already know that the toughest questions are often about what happens “if.” What happens if one of you dies? Who takes over their shares? How do you avoid being in business with a spouse, children, or heirs who never planned to be owners?

A buy–sell agreement spells out what happens to an owner’s interest if they die, become disabled, or leave the business. But the agreement is only as strong as your ability to fund it. Whole life insurance gives you a way to do that with both certainty and flexibility.

You can use whole life policies to:

- Provide a death benefit that funds the buyout of a deceased owner’s shares, so you can keep control of your company and avoid forced sales or fire‑drill financing.

- Build cash value that may be available (subject to the policy terms) for planned ownership transitions, such as retiring a partner gradually or restructuring the ownership over time.

By combining a well‑drafted buy–sell agreement with whole life insurance, you give yourself a clear, funded plan for continuity. That protects you, your partners, your families, and the long‑term value of the business you’re building.

C. Executive and Owner Benefits: Reward and Retain Your Talent

In a competitive talent market, you need ways to reward and retain key people beyond salary and standard benefits. Whole life insurance can help you design executive and owner benefits that are both meaningful and tied to long‑term loyalty.

You might use whole life policies as part of:

- Executive bonus plans, where you pay the premium on a policy owned by the executive, creating a valuable benefit that can supplement their long‑term financial security.

- Supplemental retirement arrangements, where the policy’s potential cash value becomes part of a broader strategy to provide future income or benefits to key individuals.

For you as an owner, a personally or business‑owned whole life policy can also become part of your own long‑term strategy—helping you protect your family, support a future exit, or create options for income later in life, all while maintaining protection during your working years.

When you design these benefits carefully, you’re not just handing out perks. You’re tying meaningful, long‑term value to the ongoing success of your company, giving key people one more reason to stay, perform, and think like owners alongside you.

Support Long-Term Growth and Opportunity

Stability doesn’t mean standing still. You still want to grow, invest, and seize opportunities—you just want to do it without putting your entire business at risk. When you use whole life insurance strategically, you can support your long‑term growth while adding a layer of predictability to your planning.

One way you can do this is by using the policy’s cash value as a flexible financial tool. Over time, as your cash value builds, you may be able to access it through policy loans or withdrawals, subject to the contract terms. That access gives you an additional option when you need capital—whether traditional lending is tight, or you simply want to avoid taking on more outside debt. Used carefully, this lets you lean on a pool of value you’ve been building for years instead of scrambling for financing at the last minute.

You can also use your policy as part of your broader financing strategy. In some cases, lenders may allow you to use the policy’s cash value as collateral, which can strengthen your position when you apply for a loan. That can help you negotiate from a place of greater confidence when you:

- Invest in new equipment or technology

- Open a new location or expand your footprint

- Acquire a competitor or a complementary business

- Make a strategic hire or invest in a major marketing push

Imagine you’ve built a successful closely held business and see an opportunity to acquire a smaller competitor at a discount during a downturn. Instead of relying only on bank financing or draining your operating cash, you might tap into the cash value of a whole life policy—either directly or as collateral—to close the deal on terms that work for you. You still need to manage the policy carefully, but you’ve given yourself an additional way to say “yes” to the right opportunity.

When you integrate whole life insurance into your long‑term strategy this way, you’re not just protecting against worst‑case scenarios. You’re also giving yourself more control over how and when you pursue growth, so you can align each major decision with both your current reality and your long‑range goals.

Risk Management and Common Misconceptions

As you look at whole life insurance for your business, it’s just as important to be clear about what it *isn’t* as what it is. You protect yourself best when you understand both the strengths and the limitations of the tool you’re considering.

First, whole life is not a replacement for all your other investments or planning strategies. You aren’t choosing between whole life and growth assets like your business, your retirement accounts, or your investment portfolio. Instead, you’re deciding whether to add a long-term, guaranteed element alongside those other pieces. If you expect whole life to deliver stock‑like returns or to solve every planning issue, you will almost certainly be disappointed.

You also need to be realistic about liquidity. In the early years of a policy, cash value grows slowly, and surrender charges can reduce what you can access if you decide to walk away. That means whole life works best for you when you have a long time horizon and you’re comfortable making a sustained commitment. If you’re likely to need every dollar back in the first few years, it may not be the right fit.

Policy loans and withdrawals can be helpful tools, but they require discipline from you. Loans accrue interest and reduce the policy’s cash value and death benefit if not repaid. If you borrow aggressively and don’t manage it, you can unintentionally weaken the very protection you set out to create. You’ll want to work with your advisor and tax professionals to understand how different access strategies could affect your coverage and your tax situation.

Finally, whole life works best when it is coordinated with the rest of your plan. You’ll want to look at it alongside your lines of credit, retained earnings, disability coverage, retirement plans, and legal agreements like your buy–sell. When you view it in that broader context, you can decide whether whole life truly adds stability for you or whether your goals can be met more efficiently with other tools you already have in place.

How to Evaluate if Whole Life Fits Your Business

Before you add whole life insurance to your business strategy, you need to be clear about what problem you’re trying to solve. That starts with stepping back and asking yourself some focused questions about your goals, your risks, and your time horizon.

Begin with your top long-term objectives. Ask yourself:

- What do you want your business to look like 10–20 years from now?

- Do you plan to sell, pass it to family, or gradually step back while others take over?

- How important is it for you to create predictable value—both for your business and for your personal financial life?

Next, look at where you’re most vulnerable. Consider questions like:

- How dependent are you on one or two key people (including yourself) for revenue, relationships, or operations?

- If something happened to one of you, do you have a clear, funded plan to keep the business running?

- Do you already have a written buy–sell agreement, and if so, is it properly funded—or is it just “paper planning”?

Then, think about liquidity and resilience:

- How do you currently build reserves for downturns or unexpected events?

- Are you comfortable with how much you rely on bank financing or lines of credit?

- Would an additional, more predictable pool of value give you more confidence in your long‑term decisions?

Once you’ve answered these questions, you’ll have a clearer picture of whether whole life might add something meaningful—or whether you’re already well covered with other tools. This is the point where you bring in your advisory team.

Sit down with a financial professional, your CPA, and your attorney to:

- Review your goals and vulnerabilities.

- Map out how a policy might be structured (who owns it, who’s insured, who’s the beneficiary).

- Examine the tax and legal implications for your specific situation.

By approaching whole life this way,as a potential fit to be evaluated, not a product to be sold,you give yourself the space to decide whether it truly supports your long‑term business goals, or whether your capital is better used elsewhere.

Implementation: Best Practices for Putting Whole Life to Work

Once you decide whole life insurance might belong in your business strategy, the way you implement it matters just as much as the decision itself. You want the policy to fit your goals, your cash flow, and your broader planning—not sit on the shelf as an isolated product.

Start by bringing in your advisory team. You don’t want to do this in a vacuum. Involve:

- A financial professional who understands both business and personal planning

- Your CPA, to review tax treatment and cash-flow impact

- Your attorney, to align policies with your legal documents (especially buy–sell agreements and ownership structures)

Together, you can clarify what you want the policy to do for you:

- Are you protecting a key person?

- Funding a buy–sell agreement?

- Building a conservative reserve?

- Providing an executive or owner benefit?

Once you’re clear on the purpose, you can design the policy around it. That means deciding:

- **Who will be insured** (you, a partner, a key employee).

- **Who will own the policy** (you personally, the business, or a trust).

- **Who will be the beneficiary** (the business, family members, or both, depending on the strategy).

- **How premiums will be funded** and how they fit into your budget.

After the policy is in place, you need to treat it like any other important business asset: monitor it and review it regularly. At least once a year, you should:

- Confirm the coverage still matches your goals and business value.

- Review policy performance and any dividends, if applicable.

- Revisit how loans or withdrawals, if you’ve used them, affect your long‑term plan.

- Update your legal documents if ownership, partners, or succession plans have changed.

By approaching implementation this way—deliberate, coordinated, and reviewed—you make sure your whole life policy actually supports your long‑term business goals, instead of just adding another line item to your expenses.

Turn Uncertainty into Long-Term Stability

When you lead a business in uncertain times, you can’t afford to rely on hope or short-term fixes. You need structures that help you protect what you’ve built, keep your options open, and stay on course even when the environment changes. Whole life insurance, when used thoughtfully, can be one of those structures.

You can use it to protect your business if something happens to you or a key person, to fund ownership transitions on your terms, and to build a conservative asset that supports your long-term strategy instead of working against it. You aren’t replacing your existing plans; you’re adding another layer of stability around them.

Your next step is simple: look at your current planning through a stability lens. Ask yourself where your business is most vulnerable—key people, succession, liquidity in a downturn—and where a guaranteed, long-term tool might help. Then bring those questions to your advisor team so you can explore whether whole life insurance belongs in your specific plan, and if so, how to structure it around your goals.

When you approach whole life this way—not as a product to buy, but as a strategy to evaluate—you give yourself one more way to turn uncertainty into long-term stability for your business and the people who rely on it.

Design a Holistic Financial Strategy: The Role of Annuities in Long-Term Business Planning

Most business owners pour everything into building their company, but far fewer have a clear, coordinated plan for turning that success into long-term personal security.

Why Holistic Planning Matters for Business Owners

You have built a business that others rely on—your team, your customers, your community. But if you are like many owners, you have invested most of your energy (and capital) into the business itself while your personal long-term plan remains more of a hope than a strategy. Revenue looks strong, the balance sheet is solid, yet the question lingers: “Will this actually translate into the life I want later?”

The challenge is not effort or ambition. The challenge is fragmentation. You have business finances in one lane, personal investments in another, taxes in a third, and maybe some insurance or retirement accounts scattered around them. Each decision might make sense on its own, but without a cohesive strategy, it is difficult to know whether everything is truly working together for your long-term goals.

This is where holistic financial planning becomes essential. A holistic approach connects business value, personal wealth, retirement income, risk management, and legacy planning into one coordinated strategy. Instead of choosing products first and trying to fit them into your life later, you start with your goals—how you want your future to look—and then design solutions that support that picture.

Within this broader strategy, annuities are not a magic answer or a one-size-fits-all product. They are one potential tool that can help turn uncertain future cash flows into stable, predictable income. Used thoughtfully, annuities can support a more resilient plan for both your business transition and your life after you step away from the day-to-day operations.

What a “Holistic Financial Strategy” Really Means for You as a Business Owner

When you think holistically about your finances, you stop treating your business, your personal savings, your taxes, and your retirement as separate projects. Instead, you look at how every decision in your business affects your life outside the business—and vice versa. You ask, “If I keep doing what I’m doing, will this reliably support the life I want 10, 20, or 30 years from now?”

A holistic financial strategy starts with your goals, not with products. You clarify what you want your future to look like: when you want to step back from the business, how much flexibility you want, what lifestyle you want to support, and what you hope to leave for family or causes you care about. From there, you align business cash flow, investments, retirement accounts, insurance, and tax planning so they all move in the same direction.

For you as an owner, this means balancing three priorities: growth, protection, and predictability. You still want your assets to grow, but you also want to protect what you have built and create a base of income you can count on regardless of market conditions or business outcomes. A holistic plan helps you see which risks you are comfortable keeping and which risks you want to transfer or reduce.

This is also why “product-first” advice often falls short for business owners. When someone leads with a specific investment or insurance product, they are trying to solve a small piece of the puzzle without seeing the full picture of your business, your taxes, your family, and your long-term plans. A truly holistic approach starts with your unique situation and then uses tools—annuities included—only where they clearly support your bigger strategy.

Where Annuities Fit in the Big Picture

When you hear the word “annuity,” you might think of a complicated insurance product. At its core, an annuity is simply a contract where you give an insurance company money—either all at once or over time—and in return, you receive certain guarantees.

Strategic Use Cases for Annuities in Your Business Planning

When you look at annuities through a strategic lens, they stop being “just another product” and start becoming tools you can use in very specific parts of your plan. Here are four key ways you might use them.

Strengthen Your Own Retirement Security

As a business owner, a lot of your net worth may be tied up in your company. You might be counting on a future sale or buyout to fund your lifestyle later. Annuities can help you translate that uncertain future event into more predictable income.

You can use an annuity to:

- Turn a lump sum from a business sale—or surplus cash you don’t want to put at high risk—into a stream of guaranteed income for a set period or for life.

- Create a baseline of income that will arrive regardless of market conditions, business performance, or interest rates.

- Reduce the risk of outliving your assets by shifting some longevity risk to an insurance company.

This kind of structure can give you more confidence that your personal lifestyle isn’t entirely dependent on what happens to your business or the markets after you exit.

Enhance Retirement Benefits for Key Employees

Your top people help drive your company’s value, but traditional retirement plans (like a 401(k)) may not fully reward or retain them—especially if their income is higher or more variable.

You can use annuities to:

- Provide supplemental retirement benefits as part of a nonqualified plan or executive benefits package.

- Offer key employees a clearer picture of future income, which can be more tangible than just an account balance.

- Tie long-term benefits to retention, helping you keep crucial talent in place through key growth or transition periods.

By designing these benefits thoughtfully, you can support your team’s long-term security while aligning their interests with the long-term health of your business.

Support Exit and Succession Planning

When you think about stepping back from your business, timing, cash flow, and control all matter. Annuities can play a role in smoothing that transition.

You can use annuities to:

- Convert a portion of your buyout or sale proceeds into predictable income that starts when you plan to exit—or earlier if you want to phase out.

- Support a buy-sell agreement by helping ensure that future income to you (the departing owner) is reliable, even if the next generation or new owners face a rough patch.

- Structure a staged exit where you slowly reduce your involvement while still receiving a stable, guaranteed stream of income.

This can reduce pressure on the business, the successors, and you as you move from “owner-operator” to “former owner” with a new life rhythm.

Manage Risk and Create a Volatility Buffer

Even if you are comfortable with market risk and business risk, you may not want your entire future riding on both at the same time. Annuities can help you build a more stable foundation under your plan.

You can use annuities to:

- Create a reliable income floor so that your essential expenses are covered, while your other investments and business interests remain focused on growth.

- Reduce the need to sell investments—or draw too heavily from the business—during down markets or slower revenue periods.

- Balance your overall risk exposure by mixing guaranteed income with more volatile assets.

By using annuities as one piece of your strategy, you give yourself permission to keep taking smart risks in your business and portfolio, knowing that part of your future income is already secured.

Key Considerations Before You Add Annuities to Your Strategy

Before you add any annuity to your plan, you want to be clear on *why* it belongs there. The right annuity, in the wrong context, can still create friction. The more specific you are about your goals and constraints, the easier it is to see whether an annuity supports or conflicts with your broader strategy.

How to Evaluate Annuities Through a Holistic Lens

When you evaluate annuities, you want to zoom out before you zoom in. Instead of asking, “Is this a good product?” you ask, “Does this help my overall plan work better?” That shift in perspective keeps you from getting lost in features and acronyms that may not matter for your actual goals.

---

1. Start With Your Goals and Cash Flow, Not With Products

Before you look at any illustration or brochure, get clear on what you want the annuity to do for you:

- Are you trying to secure a baseline of guaranteed income at a certain age?

- Are you trying to protect part of a future business sale from market volatility?

- Are you trying to enhance retirement benefits for yourself or key employees?

When you define the job you want the annuity to perform—amount of income, start date, length of time, and level of guarantees—you can quickly see which options are aligned and which are just noise.

---

2. Map Your Entire Financial Picture First

You get the most value from annuities when you see them in the context of everything else you own and owe. Before committing, take inventory:

- Your business value and expected exit or transition timeline.

- Your existing retirement accounts (401(k), IRAs, SEP, SIMPLE, etc.).

- Your taxable investments, savings, and real estate.

- Any existing insurance or income guarantees.

This helps you decide how much of your future income truly needs guarantees and how much can reasonably stay invested for growth. An annuity should fill a gap, not duplicate what you already have.

---

3. Stress-Test Different Scenarios

A holistic view means you don’t just plan for the “base case.” You also look at what happens if life and business don’t go according to script. As you evaluate an annuity, ask how it performs if:

- You sell your business earlier or later than expected.

- Markets experience a prolonged downturn.

- Your health changes or you live much longer than you anticipated.

- You or your successors face a rough patch in the business.

If the annuity still supports your plan in those tougher scenarios—by providing steady income, reducing pressure on other assets, or protecting you from outliving your money—it may have a stronger place in your strategy.

---

4. Coordinate With Your Professional Team

Because you wear multiple hats—owner, investor, employer—you benefit from having your advisory team on the same page. As you consider an annuity, involve:

- Your CPA, to evaluate tax treatment and ownership structure.

- Your attorney, to ensure alignment with your estate plan, buy-sell agreements, or succession documents.

- Your financial planner or advisor, to integrate the annuity into your broader investment and retirement plan.

When everyone understands how the annuity is supposed to function in your life and business, you reduce the risk of unintended consequences or conflicting strategies.

---

5. Use the Annuity to Support, Not Drive, Your Plan

Ultimately, you want your life goals and business plans to drive your decisions—not the latest product, sales pitch, or market headline. When you evaluate annuities through a holistic lens, you treat them as one set of tools among many.

You ask:

- Does this annuity make my future income more reliable?

- Does it reduce a risk I care about, in a way that justifies the cost and trade-offs?

- Does it fit cleanly with my business plans, tax strategy, and legacy goals?

If you can answer “yes” to those questions, the annuity is not just a contract. It becomes a deliberate part of a coordinated strategy designed around you, your business, and the life you want your work to support.

---

1. Your Time Horizon

You first want to think about when you expect major transitions to happen:

- When do you plan to step back or exit your business?

- When will you realistically need income from your investments, not just growth?

If you still have many years before you need income, you may focus on annuities that allow for growth and later income. If you are closer to exit or already in transition, immediate or near-term income options may be more relevant. Your timing drives which type of annuity, if any, makes sense.

---

2. Your Comfort With Risk vs. Guarantees

Annuities shift certain risks—like market volatility or outliving your money—from you to an insurance company. In exchange, you often give up some liquidity, upside, or flexibility.

You want to be honest about:

- How much of your future income you want guaranteed versus exposed to market growth.

- How comfortable you are with trade-offs such as caps on returns, income riders, or restrictions on withdrawals.

The goal is not to eliminate all risk. It is to decide which risks you prefer to keep and which you prefer to transfer.

---

3. Tax Treatment and Ownership Structure

As a business owner, you need to look at annuities through both a personal and business tax lens. Depending on whether the annuity is owned by you personally or by your business, the tax treatment of contributions, growth, and withdrawals can differ.

You should consider:

- Whether premiums should be paid from business or personal funds.

- How future income will be taxed and how that fits with your broader tax strategy.

- How the annuity coordinates with your existing retirement plans (401(k), SEP, SIMPLE, etc.).

Reviewing this with your tax advisor helps you avoid surprises and make the structure work for you.

---

###4. Liquidity and Access to Funds

Annuities are designed for long-term goals, not short-term cash needs. You want to be sure that the dollars you commit to an annuity are not dollars you might need quickly for emergencies, reinvestment in the business, or new opportunities.

You’ll want clarity on:

- Surrender periods and surrender charges.

- How much you can access each year without penalties.

- Any provisions for unexpected events (health issues, long-term care, or other emergencies).

Your annuity should support your flexibility, not become a source of stress when circumstances change.

---

5. Fees, Riders, and What You’re Really Paying For

Every guarantee has a cost, whether it is visible as a fee or embedded in the contract terms. You want to understand exactly what you are paying, what you are getting in return, and whether that trade-off is worthwhile relative to your goals.

You should ask:

- What are all the internal costs and rider fees?

- What risks are these fees actually protecting you from?

- Could you achieve something similar with other tools at a lower cost, or is the guarantee worth the premium to you?

When you see annuities as part of your holistic strategy—not as isolated products—you can evaluate them more clearly. You are not asking, “Is this annuity good or bad?” You are asking, “Does this specific annuity, with these features and costs, help me move closer to the life and business outcomes I care about?”

How to Evaluate Annuities Through a Holistic Lens

When you evaluate annuities, you want to zoom out before you zoom in. Instead of asking, “Is this a good product?” you ask, “Does this help my overall plan work better?” That shift in perspective keeps you from getting lost in features and acronyms that may not matter for your actual goals.

---

1. Start With Your Goals and Cash Flow, Not With Products

Before you look at any illustration or brochure, get clear on what you want the annuity to do for you:

- Are you trying to secure a baseline of guaranteed income at a certain age?

- Are you trying to protect part of a future business sale from market volatility?

- Are you trying to enhance retirement benefits for yourself or key employees?

When you define the job you want the annuity to perform—amount of income, start date, length of time, and level of guarantees—you can quickly see which options are aligned and which are just noise.

---

2. Map Your Entire Financial Picture First

You get the most value from annuities when you see them in the context of everything else you own and owe. Before committing, take inventory:

- Your business value and expected exit or transition timeline.

- Your existing retirement accounts (401(k), IRAs, SEP, SIMPLE, etc.).

- Your taxable investments, savings, and real estate.

- Any existing insurance or income guarantees.

This helps you decide how much of your future income truly needs guarantees and how much can reasonably stay invested for growth. An annuity should fill a gap, not duplicate what you already have.

---

3. Stress-Test Different Scenarios

A holistic view means you don’t just plan for the “base case.” You also look at what happens if life and business don’t go according to script. As you evaluate an annuity, ask how it performs if:

- You sell your business earlier or later than expected.

- Markets experience a prolonged downturn.

- Your health changes or you live much longer than you anticipated.

- You or your successors face a rough patch in the business.

If the annuity still supports your plan in those tougher scenarios—by providing steady income, reducing pressure on other assets, or protecting you from outliving your money—it may have a stronger place in your strategy.

---

4. Coordinate With Your Professional Team

Because you wear multiple hats—owner, investor, employer—you benefit from having your advisory team on the same page. As you consider an annuity, involve:

- Your CPA, to evaluate tax treatment and ownership structure.

- Your attorney, to ensure alignment with your estate plan, buy-sell agreements, or succession documents.

- Your financial planner or advisor, to integrate the annuity into your broader investment and retirement plan.

When everyone understands how the annuity is supposed to function in your life and business, you reduce the risk of unintended consequences or conflicting strategies.

5. Use the Annuity to Support, Not Drive, Your Plan

Ultimately, you want your life goals and business plans to drive your decisions—not the latest product, sales pitch, or market headline. When you evaluate annuities through a holistic lens, you treat them as one set of tools among many.

You ask:

- Does this annuity make my future income more reliable?

- Does it reduce a risk I care about, in a way that justifies the cost and trade-offs?

- Does it fit cleanly with my business plans, tax strategy, and legacy goals?

If you can answer “yes” to those questions, the annuity is not just a contract. It becomes a deliberate part of a coordinated strategy designed around you, your business, and the life you want your work to support.

Bring It All Together and Your Next Step

When you step back and look at your financial life as a whole, you see more than a business, a few accounts, and some legal documents. You see the life you are building—for yourself, your family, your team, and your community. A holistic financial strategy respects that bigger picture. It starts with what you want your next chapter to look like and then aligns your business value, investments, taxes, and protections around those goals.

Within that context, annuities are not the star of the show. They are one of the supporting actors—useful when you want more certainty, predictable income, or protection against living longer than expected. When you use them intentionally, annuities can help you convert the success of your business into lasting financial security and flexibility.

Your next step is simple: take inventory and get curious. Ask yourself:

- How much of my future lifestyle do I want guaranteed, and how much am I comfortable leaving to markets and business outcomes?

- If I sold my business tomorrow, do I have a clear plan to turn that value into reliable income?

- Are there gaps in my current plan that an annuity or other tools might help fill?

From there, consider having a conversation with a planner who understands both business realities and personal goals—and is willing to start with your life, not with a product. When you approach annuities this way, you are not just buying a contract. You are designing a more intentional path from the work you are doing today to the life you want that work to support tomorrow.

Beyond CDs: Why a MYGA May Be a Smarter Home for Your Safe Money

A portion of that “safe money” could be working harder for you without taking on stock market risk

Why Savers Are Looking Beyond CDs

If you’re a conservative saver, chances are you’ve relied on certificates of deposit (CDs) for years. They’ve felt familiar and safe: you lock up your money, you know your rate, and you don’t have to think about it again until maturity. But lately, many people are opening those renewal notices and wondering, “Is this really the best I can do with my safe money?”

CD rates often move in step with headlines, but not always in a way that works for you. In some environments they barely outpace inflation—if at all—leaving your “safe” dollars quietly losing purchasing power over time. At the same time, that interest is usually taxed every year, even if you’re just letting it roll and don’t actually spend it.

On top of that, life has likely become more complex. You may be thinking less in terms of “one CD at a time” and more in terms of specific goals: bridging the years until retirement, covering future healthcare expenses, or simply creating a dependable income floor so market swings don’t keep you up at night. CDs are straightforward, but they’re not always flexible or efficient when you zoom out to the bigger picture.

That’s where MYGAs—Multi‑Year Guaranteed Annuities—come in. They’re not a replacement for every CD, and they’re not right for every dollar you have in the bank. But for a portion of your safe money, a MYGA can offer a combination of guaranteed rates and tax advantages that many savers don’t realize is available. In the rest of this article, we’ll walk through how MYGAs work, how they compare to CDs, and when they may be a smarter home for the money you absolutely cannot afford to put at risk.

What Is a MYGA?

A Multi‑Year Guaranteed Annuity (MYGA) is a type of fixed annuity issued by an insurance company. Think of it as a *“CD-like” contract with an insurer instead of a bank.*

At a basic level, here’s how a MYGA works:

You make a lump‑sum deposit.

This is typically money you want to keep safe and don’t need to touch for several years.

You choose a guarantee period.

Common terms are 3, 5, 7 or even 10 years. During that time, the insurance company locks in a **fixed interest rate** for you.

Your money grows at that rate every year.

Unlike a CD at the bank, you **don’t pay taxes on the interest each year** (unless it’s in a taxable account and you take withdrawals). The growth inside the MYGA is **tax‑deferred**. You pay taxes later, when you take the money out.

At the end of the term, you have options.

You can typically renew into a new term, move the funds to another annuity, or take your money out (subject to the contract’s rules and any tax considerations).

Just as important is what a MYGA is not

- It is **not a bank CD** and is **not FDIC-insured**. Your guarantees come from the insurance company, so the company’s financial strength matters.

- It is **not a variable annuity** and **not tied to the stock market**. You’re not chasing market returns; you’re trading that upside for a clear, contractually guaranteed rate.

- It is **not a checking account or emergency fund.** MYGAs are meant for money you can commit for a period of years, not for everyday spending.

If you strip away the jargon, a MYGA is simply a **contract that exchanges your lump sum for a known interest rate over a defined period, with tax‑deferred growth as a key extra benefit. For many savers who like the predictability of CDs but want more efficiency from their “safe money,” that combination can be worth a closer look.

MYGA vs. CD: Side‑by‑Side Comparison

When you put a MYGA next to a CD, they *look* similar: both are designed for safety and predictability. But under the hood, there are important differences that can affect how much you earn, how you’re taxed, and how flexible your money really is.

A. Safety and Guarantees

CDs

- Issued by banks or credit unions.

- Protected by **FDIC or NCUA insurance** up to legal limits per depositor, per institution, per ownership category.

- Your principal and stated interest are guaranteed by the bank; the government backstop applies within coverage limits.

MYGAs

- Issued by **insurance companies**, not banks.

- Backed by the **claims‑paying ability of the insurer**, not FDIC or NCUA.

- Each state has a **guaranty association** with its own rules and coverage levels, but this protection is different from and not identical to FDIC insurance.

- Because of this, choosing a **financially strong insurer** is essential.

Both CDs and MYGAs are designed as “safe money” tools, but they rely on different types of guarantees and regulators. CDs lean on bank and federal backing; MYGAs lean on insurer strength and state oversight.

B. Interest Rates and Term Options

CDs

- Terms commonly range from a few months to 5 years.

- Rates can be attractive in certain rate environments, but they are usually offered in a narrow range of terms.

- Banks may offer short‑term promotional rates that look good initially but drop at renewal if you’re not paying attention.

MYGAs

- Common guarantee periods are 3, 5, 7, or 10 years.

- In many markets, MYGA rates can be **competitive with or higher than** similar‑term CDs because insurers can invest differently than banks.

- You lock in a single fixed rate for the entire guarantee period, which can be helpful for planning.

The takeaway: if you’re comfortable committing funds for several years, a MYGA can sometimes offer a stronger rate than a comparable CD term.

C. Tax Treatment

This is one of the clearest distinctions between CDs and MYGAs.

CDs

- Interest is typically **taxable each year** in a taxable account, even if you let it compound and do not withdraw it.

- You’ll usually receive a 1099 for the interest, and it adds to your current‑year taxable income.

MYGAs

- Growth is tax‑deferred in a non‑qualified account.

- You do not pay taxes on interest each year as it accrues; taxes are due when you take withdrawals or when the contract pays out.

- This deferral can allow your money to compound more efficiently over time, especially if you don’t need the interest for current income.

If you’re reinvesting your CD interest anyway, that yearly taxation can be a quiet drag. For “later” dollars that can sit and grow, MYGA tax deferral can be a meaningful advantage.

D. Liquidity and Access to Funds

CDs

- You can usually access your money before maturity, but you’ll pay an **early withdrawal penalty** (often several months of interest).

- Some banks offer “no‑penalty CDs,” but typically at lower rates.

MYGAs

- Designed to be held for the full term; early withdrawals can trigger surrender charges and, if you’re under age 59½, possible IRS penalties on gains.

- Many MYGAs include limited “free withdrawal” provisions (for example, up to 10% of the contract value per year) after the first year, but the specifics vary by contract.

- Because of the commitment, MYGAs are best used for money you truly can set aside for several years.

In practice, CDs often provide slightly easier access (with a known interest penalty), while MYGAs typically require a firmer time commitment but can reward that commitment with potentially higher, tax‑deferred growth.

When a MYGA May Be a Smarter Choice Than a CD

There are plenty of situations where a simple CD still does the job. But if you’re like many savers I talk with, you’re starting to feel that “good enough” with your safe money may not actually be good enough anymore. That’s often when a MYGA starts to make more sense.

Imagine you’re staring at a CD renewal notice. The rate is better than it was a few years ago, but it still feels underwhelming—especially when you realize you’ll owe taxes on that interest every single year. You don’t need the income right now; you’re just rolling it forward. In that scenario, a MYGA can give you something different: the ability to lock in a competitive fixed rate for several years **and** let the growth accumulate tax‑deferred. You’re still staying conservative, but you’re being more deliberate about how that conservative money grows.

A MYGA also starts to shine when you’re thinking in terms of timelines rather than just products. Maybe you know you won’t need a particular chunk of money for five or seven years—perhaps it’s earmarked for the early years of retirement, a future down payment, or a grandchild’s education. A CD can cover part of that window, but you may find yourself rolling from one short-term CD to another, never quite sure what rate you’ll get next. With a MYGA, you choose a term that lines up with when you’ll need the money and you know, in advance, exactly what that portion will grow to if you leave it alone.

You might also be at a stage of life where “sleep-at-night money” matters more than chasing returns. Maybe you have some investments in the market, and you’re comfortable with that, but you want a portion of your portfolio that simply does its job quietly in the background. In that case, using a MYGA for part of your safe bucket can give you the comfort of a guaranteed rate over multiple years, without asking you to monitor the market or constantly shop CD specials. It becomes a stabilizing anchor while the rest of your plan does the heavy lifting.

For many people, the real turning point is when they realize their CDs aren’t just isolated accounts; they’re pieces of a bigger strategy. If you’re reinvesting interest instead of spending it, if you can genuinely commit some dollars for more than a couple of years, and if you’d like those dollars to work a bit harder without taking market risk, then a MYGA deserves a seat at the table next to your CDs. It won’t replace every CD, and it shouldn’t. But for certain goals and timelines, it can be a smarter, more efficient home for a portion of your safe money.

Key Risks and Trade-Offs to Understand

As attractive as a MYGA can be, it’s not a magic upgrade button for every dollar you have in CDs. Before you move any money, you want a clear-eyed view of the trade-offs. Think of this as your “reality check” so you’re choosing deliberately, not just chasing a higher rate.

The first and most important question is time. A MYGA really only makes sense for money you can live without for the full length of the contract. If you lock into a 5- or 7-year MYGA and then need a large chunk of that money in year two, you could face surrender charges from the insurer—and, if you’re under 59½ and taking out gains, potential IRS penalties as well. Some contracts let you take out a limited amount each year without penalty, but that’s usually not a substitute for true liquidity. In other words, you don’t want to use MYGAs for your emergency fund or for “maybe I’ll need it soon” money.

You also have to be comfortable with the fact that a MYGA is an insurance product, not a bank deposit. With a CD, you lean on FDIC or NCUA insurance. With a MYGA, you’re relying on the financial strength of the insurance company and the protections of your state’s guaranty association, which work differently and have their own coverage limits and rules. That’s why the insurer’s ratings and balance sheet matter. If you’re used to thinking “any bank CD is basically the same,” shifting to evaluating insurer quality is a mental adjustment.

There’s also a trade-off in simplicity and flexibility. A CD at your bank is straightforward: you see it in your online banking, you know the penalty if you break it, and renewal is usually a one-click decision (for better or worse). A MYGA comes with a contract, specific provisions, and more moving parts: free-withdrawal allowances, surrender schedules, renewal options, and potential tax treatment quirks if you annuitize later. None of this is inherently bad, but it does mean you need to slow down, read (or have someone walk you through) the fine print, and be honest about how much complexity you’re willing to manage.

Finally, you want to remember that CDs still have a role. If you know you’ll need money in 6–18 months for a move, a car, or a big life event, a short-term CD, or even just a high-yield savings account, may be the better fit. MYGAs tend to make more sense for “later” dollars with a clear multi-year horizon and no expected interruptions. If you force a MYGA to do a short-term job, you’re fighting the design of the product, and that’s when the trade-offs start to hurt instead of help.

If you keep these risks and trade-offs in mind, you’re far less likely to be surprised later. The goal isn’t to talk yourself out of a MYGA or into one—it’s to match the tool to the job, so you know exactly what you’re gaining and exactly what you’re giving up when you move beyond CDs.

How to Decide: CD, MYGA, or a Mix of Both?

When you come to this crossroads—renew the CD, move to a MYGA, or blend the two—it helps to step back from rates and think about purpose first. Every dollar you’ve saved has a job. Some dollars are there to cover the next curveball life throws at you. Others are quietly waiting in the wings for a known goal: bridging the early years of retirement, funding a move, helping adult children, or simply giving you the confidence to stay invested elsewhere. How you answer the “CD or MYGA?” question depends on which job you’re trying to fill.

Start by asking yourself a simple timing question: When do I realistically need this money? If the honest answer is “sometime in the next year or two, and I’m not sure exactly when,” that leans you toward keeping things simple and liquid like shorter‑term CDs or high‑yield savings. If, instead, you can point to a date three, five, or seven years down the road and say, “That’s when I’ll actually need this,” then a MYGA starts to come into focus. You’re trading some day‑to‑day flexibility for the ability to lock in a rate and, in a taxable account, let the growth compound without an annual tax bill.

Then consider how much flexibility you need *emotionally*, not just mathematically. Some people like knowing they can walk into a bank (or log into an app) and cash out a CD, even if they never do. Others are comfortable with a firmer commitment if it means their plan is clearer and their money works harder. If the idea of surrender charges keeps you up at night, that’s important information. In that case, you may decide a MYGA is best used for a smaller slice of your safe money, while CDs handle the part you want to feel fully “reachable.”

You don’t have to choose one or the other. In fact, many people are best served by a mix. You might keep a layer of short‑term CDs or savings for near‑term needs and “psychological comfort,” and then use a MYGA or even a ladder of MYGAs for the money you truly won’t touch for several years. That way, you’re not forced into an all‑or‑nothing decision. Your liquid dollars stay liquid; your longer‑horizon dollars get the potential benefit of higher, tax‑deferred growth.

Finally, be honest about how much time and attention you want to spend on this part of your financial life. If you enjoy shopping CD specials every few months and don’t mind tracking multiple renewal dates, that’s one approach. If you’d rather make a thoughtful decision now and not revisit it every year, then carefully chosen MYGAs can simplify your world for a while. The “right” answer isn’t about what’s popular; it’s about aligning each bucket of money with its timeline, its purpose, and your tolerance for complexity and commitment.

Real-World Example (Hypothetical Case Study)

To see how this works in practice, imagine someone a lot like you.

Let’s say you’re in your early 60s, we’ll call you Maria. You’re a few years from retirement, and over time, you’ve built up $200,000 in various CDs. They’ve always felt safe and familiar. But now several of them are maturing in the coming year, and as you look at renewal options, you’re torn. You don’t want to gamble this money in the market—but you also don’t want it sitting in low‑yield CDs forever.

When we zoom out, you realize this $200,000 really has two different jobs:

- About $60,000 is earmarked for near‑term needs: helping a child with a home down payment, a possible car replacement, and some home repairs in the next 2–3 years.

- The remaining $140,000 is money you don’t expect to touch until you’re well into retirement. You’d like it to grow steadily and be there when you’re ready to supplement your income.

If you just roll everything into new CDs, you’ll preserve the simplicity you’re used to, but you’ll also keep paying tax on interest every year and accepting whatever rates the bank offers when each CD renews. Nothing is “wrong” with that, but it doesn’t fully match what you’ve told yourself you want: safety, plus a bit more efficiency and clarity.

So instead, you split the strategy.

You keep the $60,000 in a mix of shorter‑term CDs and a high‑yield savings account. That money stays fully in your comfort zone: easy to reach, simple to understand, and there for any life surprises or planned expenses in the next few years. You know you might give up a little yield compared to a longer‑term option, but the access is worth it.

For the other $140,000, you decide you’re willing to commit for longer. After looking at different options, you choose a ladder of MYGAs—for example, part in a 3‑year contract, part in a 5‑year, and part in a 7‑year. Each piece has a clearly stated, fixed interest rate and a known maturity date that lines up with stages of your retirement. Because you don’t need this money right away, you can take advantage of tax‑deferred growth, letting the interest compound quietly in the background.

Nothing about your risk profile has changed: you’re still keeping this money in conservative, guaranteed vehicles. But now your plan is more intentional. The dollars you might need soon are in places you can reach quickly. The dollars you truly won’t touch for years are working a bit harder in MYGAs, without sending you a new tax bill every year.

If you picture yourself in Maria’s shoes, you can see the shift. You’re no longer just renewing whatever CD happens to be maturing. You’re matching each pool of money to a job, a timeframe, and the right tool—sometimes that’s a CD, sometimes it’s a MYGA, and often it’s a mix of both.

How My Financial Service Fits In

When you’re deciding what to do with your CDs, it can feel like you’re being asked to make a technical decision about interest rates and product names. But underneath all of that, what you’re really trying to do is match your money to your life. That’s where I come in.

I don’t start with a product—CD or MYGA. I start with you. We look at what each dollar is meant to do: which part of your savings needs to stay liquid for surprises, which part is there to create calm and stability in retirement, and which part is simply waiting for the right opportunity. Once we’ve mapped that out, it becomes much easier to see where a traditional CD is still the best fit and where a MYGA might quietly do a better job in the background.

My role is to translate the fine print into plain English so you can make choices confidently. When we compare a CD and a MYGA, we’re not just lining up rates; we’re talking honestly about taxes, time commitments, penalties, and what it feels like to have your money in each place. If a MYGA would add unnecessary complexity or tie up funds you’re likely to need, I’ll tell you that. If it could give a portion of your safe money more efficient, tax‑deferred growth without changing your risk comfort, I’ll explain how—and just as importantly, where its limits are.

From there, we can design something that fits your life rather than forcing your life to fit a product. That might mean keeping a base layer of CDs and high‑yield savings for near‑term needs, and then building a simple MYGA ladder for dollars you truly won’t touch for several years. Or it may mean confirming that, for now, the best answer is to renew a CD and revisit the conversation later. The point is not to chase whatever is new, but to be intentional.

Ultimately, my goal is that you walk away with a clear picture: which accounts are for now, which are for later, and why each is where it is. When you can see how CDs and MYGAs work together in service of your larger goals, you’re no longer just renewing something because it’s what you’ve always done. You’re making a deliberate choice about the home you give your safe money. You have a partner alongside you to keep that plan aligned with your life as it changes.

New Job, Old 401(k): A Step‑by‑Step Guide to Your Best Move

Changing jobs? Your old 401(k) shouldn’t be an afterthought.

You just landed a new job, updated your LinkedIn headline, and started onboarding—but there is still one loose end from your old role: your 401(k). What happens to that account now? Does it just sit there? Should you move it? And if so, where?

The choices you make with your old 401(k) can have a real impact on your long‑term retirement picture. You worked hard for that money, and you want it to keep working hard for you, not get lost in the shuffle of a career move. The good news is that you have several options—and with a little clarity, you can choose the one that fits your goals instead of guessing or doing nothing by default.

In this article, you will walk through the main paths you can take with an old 401(k) when you change jobs: leaving it where it is, rolling it into your new employer’s plan, moving it to an IRA, or cashing it out. You will see how each option works, the trade‑offs to consider, and how to align your choice with your broader financial life, so your next career step also becomes a step toward a stronger retirement.

First Things First: Take Inventory

Before you decide what to do with your old 401(k), you need a clear picture of what you already have. Think of this as your financial “check‑in” before you make any moves.

1. Locate your old 401(k)

Start by confirming where your account is held. You can:

- Look at your last 401(k) statement for the provider’s name and website.

- Search your email for “401(k,” “retirement plan,” or your former employer’s name.

- Call your old HR department if you are not sure which company manages the plan.

2. Log in and review the basics

Once you know where the account is, log in or call the plan provider to review:

- **Current balance:** How much is in the account today.

- **Vesting status:** How much of the employer match you actually own.

- **Investment mix:** Which funds or options you are invested in now (for example, target‑date funds, index funds, or a mix of stock and bond funds).

- **Fees and expenses:** Look for plan administration fees and the expense ratios on your investments. Even small differences in fees can add up over time.

3. Check for outstanding loans

If you borrowed from your 401(k), find out:

- Whether the loan is still outstanding.

- What happens to the loan now that you have left the company.

In many cases, leaving your job can accelerate the loan repayment or cause the remaining balance to be treated as a taxable distribution if you do not repay it in time.

4. Gather your documents in one place

Download or save:

- Your most recent statement.

- A summary of your investment options and fees.

- Any loan information, if applicable.

Keeping these details together makes it easier to compare your old 401(k) with your new employer’s plan or an IRA. Once you have this inventory, you are ready to evaluate your options with a clear, informed view instead of guessing.

Option 1 – Leave Your 401(k) With Your Former Employer

Imagine you are a few weeks into your new job. You are settling into a new routine, learning new systems, meeting new colleagues. In the middle of all that, the idea of moving your old 401(k) may feel like one task too many. So you consider the simplest path: just leaving the account where it is.

In many plans, if your balance is above a certain minimum—often $5,000—you are allowed to keep your money in your former employer’s 401(k) even after you leave. That means your investments stay in place, your money remains in the market, and you do not have to make an immediate decision. You log in with the same provider, you see the same funds, and nothing appears to change except your job title.

Leaving the account where it is can offer some real benefits. Your old plan may give you access to low‑cost, institutional‑class funds that are not available in a typical retail account. You may feel comfortable with the investment lineup you already chose, especially if you are in a target‑date fund that automatically adjusts your mix of stocks and bonds as you approach retirement. In other words, you can keep your long‑term strategy in place without creating more paperwork during an already busy transition.

But there is another side to the story. As you change jobs over time, you can end up with a trail of old 401(k)s behind you—one at each employer. Each account has its own website, its own statement, its own list of funds. You intend to keep track of them all, but life gets busy. Years later, you may find it harder to see your overall retirement picture clearly because your savings are scattered and you are not reviewing each plan regularly.

You also need to look closely at the quality and cost of your old plan. Some 401(k)s are built with low fees and strong investment options; others are more limited or more expensive. If your former employer’s plan has higher fees or a narrow lineup of funds, leaving your money there just because it is easy today could cost you in long‑term growth. The “do nothing” option feels simple in the moment, but it is still a decision—with trade‑offs.

As you consider leaving the account where it is, you are really weighing convenience against control. You keep things familiar and avoid immediate paperwork, but you may accept less flexibility and a more fragmented retirement plan. If you think you might change jobs again, or you already have more than one old 401(k), this is a signal to pause and ask whether leaving the money behind supports the kind of organized, intentional retirement strategy you want.

Option 2 – Roll Your Old 401(k) Into Your New Employer’s Plan

Picture this: you are sitting at your kitchen table with two sets of login credentials—one for your old 401(k) and one for your new employer’s plan. You are already juggling a new role, new benefits, and a new schedule. The idea of managing two separate retirement accounts on top of everything else feels like one more thing to keep track of.

That is often when rolling your old 401(k) into your new employer’s plan starts to sound appealing. Instead of scattered accounts, you imagine logging into a single dashboard and seeing all your workplace retirement savings in one place. One password. One statement. One set of investment options to review.

Rolling over your old 401(k) into your new plan is essentially a transfer. You ask your new plan provider to pull the money from your old plan and deposit it directly into your new 401(k). You do not take possession of the funds; they move from one tax‑advantaged account to another. When it is done correctly as a “direct rollover,” you avoid taxes and penalties, and your retirement savings stay fully invested for the future.

This option can be especially attractive if your new employer offers a strong plan: low‑cost index funds, a diversified investment menu, maybe even helpful tools or advice. You gain the simplicity of having one main retirement account at work, which makes it easier to check your progress, rebalance your investments, and see whether you are on track for your goals. It can also make things cleaner later, when you are planning withdrawals in retirement.

There are other potential benefits too. Employer plans generally come with built‑in protections under federal law, which can matter if you ever face legal or creditor issues. You also keep your savings inside a familiar structure—your workplace retirement plan—rather than opening a separate account somewhere else. If you prefer a more “plug‑and‑play” setup, this can feel more comfortable than managing an account on your own.

But just as with leaving money in your old plan, there are trade‑offs. Before you decide to roll over, you need to look closely at your new 401(k). Are the fees reasonable? Are the investment options broad enough for the strategy you want—such as a mix of index funds, bond funds, and maybe a target‑date option? If your new plan is more expensive or more limited than your old one, moving your money could reduce your flexibility and quietly increase your costs over time.

You also want to check whether there is a waiting period before you are allowed to roll money in. Some companies require you to work a certain number of days or complete a probationary period before you can consolidate old accounts into the new plan. During that time, your old 401(k) will stay where it is, and you will need to keep track of both accounts for a while.

In the background of this decision is a bigger question: how much do you value simplicity? If you like having one main hub for your retirement savings, rolling into your new employer’s plan can help you feel more organized and more in control. You log into one account and see a cleaner, more unified picture of your future.

On the other hand, if your new plan is not as strong as your old one, or if you want more investment choices than your employer offers, you may decide that simplicity alone is not enough. In that case, you might keep the old plan or look ahead to the option of rolling your 401(k) into an IRA instead.

When you step back, rolling into your new employer’s plan is really about trading multiple moving parts for a single, streamlined structure—as long as the quality of that structure supports the retirement you are working toward.

Option 3 – Rolling Your Old 401(k) Into an IRA

Now imagine a different scene. You are not on your company benefits portal at all—you are on the website of a financial institution you chose, comparing IRA options. Instead of a pre-set list of funds from an employer plan, you see a wide open menu: index funds, ETFs, bond funds, even individual stocks if you want them. This is what it looks like when you decide to move your old 401(k) into an IRA.

Rolling your 401(k) into an IRA is like moving from a fixed menu to an à la carte restaurant. You still keep the tax advantages of a retirement account, but you have much more control over how your money is invested, where you hold the account, and what it costs. You choose the provider, you choose the investment strategy, and you decide how hands-on or hands-off you want to be.

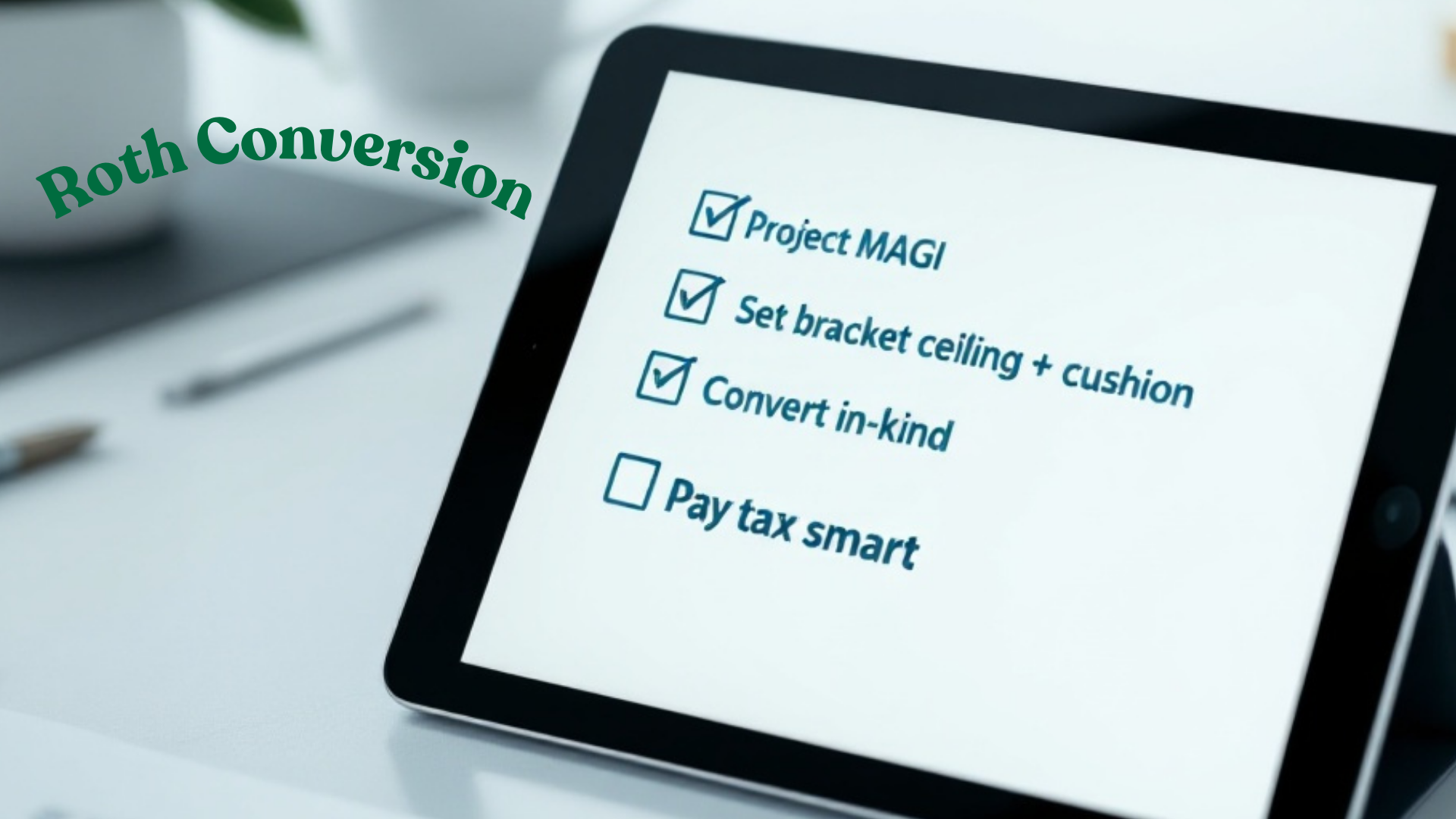

As you explore this option, you will likely encounter two main types of IRAs: Traditional and Roth. If you roll your old 401(k) into a Traditional IRA, you generally keep the same tax-deferred status your money already has. You do not pay taxes at the time of the rollover, and your investments can continue to grow tax-deferred until you withdraw them in retirement. A Roth IRA works differently. With a Roth, you pay taxes now in exchange for the potential of tax-free withdrawals later—if you follow the rules. If you convert pre-tax 401(k) dollars into a Roth IRA, you will typically owe income taxes on the amount you convert in the year of the rollover.

This is where your personal situation starts to matter. You may ask yourself: Do you expect your tax rate to be higher or lower in retirement? Do you have cash available to cover any taxes if you are considering a Roth conversion? Are you looking for flexibility around withdrawals later on? The IRA path gives you room to tailor your decision to your broader financial picture rather than simply accepting whatever structure your employer offers.

You might find the idea of broader investment choices appealing. Maybe you want a simple, low-cost index fund approach. Maybe you prefer a target-date fund but with a specific provider your employer plan does not offer. Or perhaps you want professional management through an advisor who can build and monitor a portfolio for you. In an IRA, you have the flexibility to build the strategy that fits your risk tolerance, time horizon, and goals, rather than working within the limits of a single 401(k) menu.

Along with that flexibility, though, comes more responsibility. In an IRA, you no longer have an employer screening and selecting a short list of options for you. You—or an advisor you choose—are responsible for making sure your investments stay diversified, your risk level matches your goals, and your plan stays on track over time. If you like having more say and are willing to engage with your investments (or delegate to a professional), this can feel empowering. If you prefer a more “set it and forget it” approach without much decision-making, it can feel like too much choice.

You also want to be aware of differences in protections and rules. Employer plans like 401(k)s typically offer strong protections under federal law if you ever face bankruptcy or certain legal claims. IRAs may be protected differently, depending on your state. Required minimum distributions (RMDs) also come into play later in life, and the rules can differ for Traditional and Roth accounts. None of this is necessarily a reason to avoid an IRA, but it is a reminder to look beyond just investments and fees.

As you weigh this option, you might picture your future self trying to see your entire retirement plan on one screen. Would you feel more in control if your old 401(k) lived in an IRA you chose and understood? Do you want the freedom to adjust your strategy over time without changing jobs? Rolling into an IRA is about owning more of the decisions around your retirement savings—where they are, how they grow, and how they eventually support you.

If that level of control and customization sounds like a good fit for you—and you are comfortable taking on (or delegating) the extra responsibility—moving your old 401(k) into an IRA can be a powerful way to align your retirement savings with the rest of your financial life.

Option 4 – Cashing Out Your 401(k)

Picture this moment: you have just left your job, and a letter arrives in the mail or an email pops up in your inbox. It reminds you about your old 401(k) and mentions something that catches your eye—a cash-out option. Suddenly, the idea of a lump sum of money in your bank account sounds tempting. You start thinking about paying off a credit card, catching up on bills, or giving yourself a financial “reset” between jobs.

On the surface, cashing out feels simple. You ask for the money, the plan sends you a check, and you can use it however you want. But as you look closer, you begin to see that this is not just a payout—it is a trade of long‑term retirement dollars for short‑term cash. And that trade comes with real costs.

When you cash out a pre‑tax 401(k), the amount you withdraw is generally treated as taxable income for the year. The plan may withhold a portion of the money upfront for federal taxes, but your actual tax bill will depend on your total income and tax bracket. If you are under age 59½, there is usually an additional early withdrawal penalty on top of regular income taxes. By the time taxes and potential penalties are taken into account, the amount that lands in your checking account can be much smaller than the number you saw on your statement.

Beyond the immediate tax hit, there is a quieter cost that is easy to overlook: lost future growth. If you leave the money invested in a retirement account, those dollars have years—or even decades—to grow and compound. When you cash out, you are not just taking today’s balance; you are giving up what that balance could have become over time. Future‑you loses a portion of your retirement cushion so present‑you can solve a problem or satisfy a need right now.

Of course, life is not always neat and orderly, and sometimes you may feel like you have no good options. Maybe you are facing a job gap, medical bills, or urgent expenses with no emergency savings to draw from. In those situations, cashing out can feel like the only way to keep your head above water. If you find yourself there, it can help to pause and ask a few questions before you decide:

- Have you explored other sources of cash—such as temporary income, a short‑term budget adjustment, or lower‑cost borrowing?

- Could you withdraw only what you absolutely need instead of the entire account balance?

- Do you understand how much of your withdrawal you will actually keep after taxes and penalties?

When you walk through those questions honestly, you may still decide that cashing out a portion of your 401(k) is necessary. If that happens, it can help to treat the decision as a last‑resort safety valve rather than a convenient windfall. The goal is to protect as much of your long‑term retirement money as you can, even while you deal with what is in front of you.

In the end, the cash‑out option is less about whether you *can* take the money and more about whether you *should*. The immediate relief of having extra cash today needs to be weighed against the long‑term cost to your future self. If you can find a way to leave your old 401(k) invested—by keeping it where it is, rolling it to your new employer’s plan, or moving it to an IRA—you give your retirement savings a chance to keep growing alongside your career, instead of stopping their progress just when time is still on your side.

How to Decide: Match the Option to Your Life Goals

By now, you may feel like you are standing at a four‑way intersection with your old 401(k): leave it where it is, roll it to your new plan, move it to an IRA, or cash it out. Each path has its own appeal, and each comes with trade‑offs. The real question is not “Which option is best in general?” but “Which option is best for *you*?”

Imagine sitting down with a cup of coffee and laying out your financial life on the table—not just your 401(k), but everything: your savings, your debt, your family responsibilities, your plans for the next few years. You are not trying to make a perfect decision; you are trying to make a decision that fits the life you are actually living.